Indian equity market has been tottering since the beginning of 2008. Equity mutual funds have lost around 40 per cent since the beginning of 2008. Seeing the volatility the question on everyone's minds is: Is this a good time to invest, or is worse yet to come? If you believe that markets will fall further, you could stay in cash.

We, however, do not believe in timing the market. Financial goals are important and it's always advisable to avoid timing the market as there's no telling how it might behave tomorrow, or the day after.

Short-term vs long-term. When will the markets rise or fall, is anybody's guess. This, however, should not change your goals. So, how do you invest in the market, ride the volatility and still reach your financial goals? The short answer is systematic investment plans.

Under SIPs, investments are a pre-specified amount, in a selected scheme and at pre-specified time periods, monthly or quarterly. Say, you invest Rs 1,000 every month in a pre-determined equity scheme, and start when its net asset value was Rs 15.

In the first month, 66.67 (Rs 1,000 / Rs 15) units are credited to your account. Say, on the first day of the following month the NAV increases to Rs 20. An additional 50 units (Rs 1,000/Rs 20) are credited to your account that day.

Further, say, on the first day of the next month, the NAV drops to Rs 12. In that case, 83.33 (Rs 1,000/Rs 12) units will be credited to your account.

In an SIP, more units will be credited when a scheme's NAV is low and fewer units when it's NAV is high.

Why SIP?

The mantra for wealth creation is to invest early and regularly irrespective of the size of the amount invested. SIPs are the ideal tool for this. The sooner you begin investing, the more time your money will have to grow because of power of compounding.

Regular, disciplined investing. If you are a salaried investor, SIPs enable you to save a fixed portion of your salary every month. You don't even need to remember your date of investment.

Just enrol in a monthly SIP and give a bank mandate to your fund; every month a fixed sum will automatically get transferred from your account to your chosen equity scheme.

Just enrol in a monthly SIP and give a bank mandate to your fund; every month a fixed sum will automatically get transferred from your account to your chosen equity scheme.

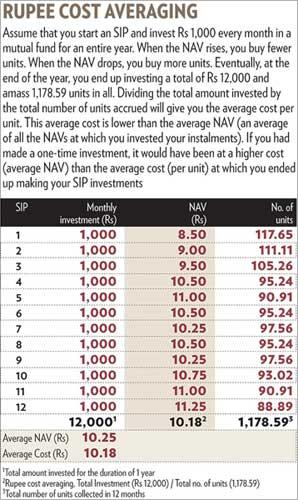

Cost averaging. By buying fewer units when the NAV is high and more units when it is low, your buying cost per unit gets averaged out. This is called rupee cost averaging (see Rupee Cost Averaging).

This helps you avoid the need to time the market. Usually, when the NAV drops, many investors don't buy additional units fearing a further drop in the market. They stay out and miss an opportunity to get units cheaper, especially if the NAV starts going up.

An SIP allows you to buy an appropriate quantity of units depending on the NAV's direction.

Rupee cost averaging doesn't work in rising markets because, in an SIP, units become more expensive as markets keep rising.

Small amounts. As an SIP entails regular investing; all you need is as low as Rs 100 a month to enrol, as against Rs 5,000 for a one-time investment. Earlier, SIPs called for a minimum investment of Rs 500, but over the past two years, competition has brought down the entry barriers. Presently, Reliance, ICICI Prudential and Lotus India MFs offer Rs 100 SIPs.

No lock-in period. Except for those in equity-linked saving schemes (ELSS), SIPs do not impose a lock-in period. If you wish to discontinue your SIP at any time, all you need to do is to inform your fund house by sending them a termination letter.

If you gave post-dated cheques when you started your SIP, your MF will return the uncashed ones. Else, if you had opted for direct debit, your payments would stop after your MF receives your termination request. Further, you can stay invested in the scheme for as long as you want even after you terminate the SIP.

How to invest in an SIP?

All MFs have predetermined dates of any given month on which an investor can make regular investments in SIPs. For instance, if you receive your salary on the first of every month, you can choose seventh or tenth of every month as your SIP date.

But if you get your salary by the month-end, the first of the following month would be the ideal, as you wouldn't want your money lying idle in the bank account for long.

MFs also provide direct debit facility with all the major banks. You can also give post-dated cheques (at least 12) to the MF.

Who should invest?

If you want steady returns and would like to avoid market volatility, SIPs are for you. But they are not suitable for short- to very short-terms. These are most suited for those who have a regular stream of inflows and would like to deploy a part of their proceeds in the market, irrespective of what level the market is at.

ELSS SIPs. Before investing in an ELSS SIP, do remember that the lock-in period for each instalment is three years. So, an amount invested on 7 July 2008 will be locked in till 6 July 2011 and the one made on 7 August 2008 will be locked till 6 August 2011.

Systematic transfer plan. But what if you have a lumpsum amount to invest? You still stagger your investments like in an SIP and make the volatility work for you through a systematic transfer plan.

In an STP you first invest a lumpsum amount in a liquid or liquid-plus fund or any other debt fund like a floating rate fund. This money will later be transferred to an equity fund of your choice within the same fund house, every day, week, month or quarter, depending on what you choose.

Your money lying in a liquid fund, pending deployment to your chosen equity fund, would fetch you higher returns than a savings bank account where you would have normally parked your surplus cash.

| Interactive |

|

1st Person: I'm not able to save regularly. I don't have the discipline.

2nd Person: Why don't you start a mutual fund SIP? You can invest a small amount every month.

1st Person: The markets are doing badly. Do you think I should stop my SIP?

2nd Person: No, because this is a chance to get units cheaper. Then, as and when the markets rise, you can make a profit. |

© 2025

© 2025